Block Inc (NYSE: XYZ)

Section: Executive Summary

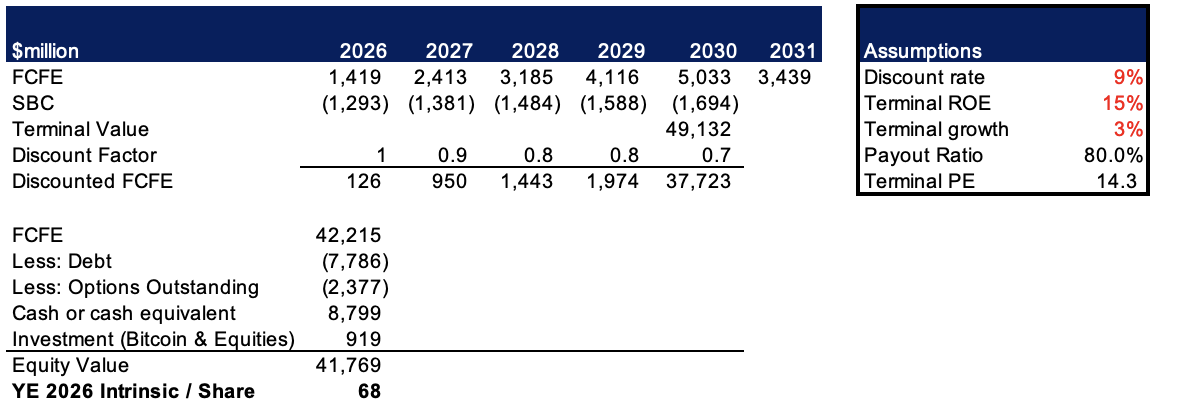

Initiate at BUY; intrinsic value $68 by YE2026 (36% upside vs. $50). Block has evolved from a payments company into a two-sided financial ecosystem and has built a highly defensible ecosystem that structurally advantages it over its peers.

Key Thesis: Block’s moat is the compounding of (1) merchant operating-system switching costs and (2) consumer velocity + habit loops, connected by an emerging closed-loop payments rail.

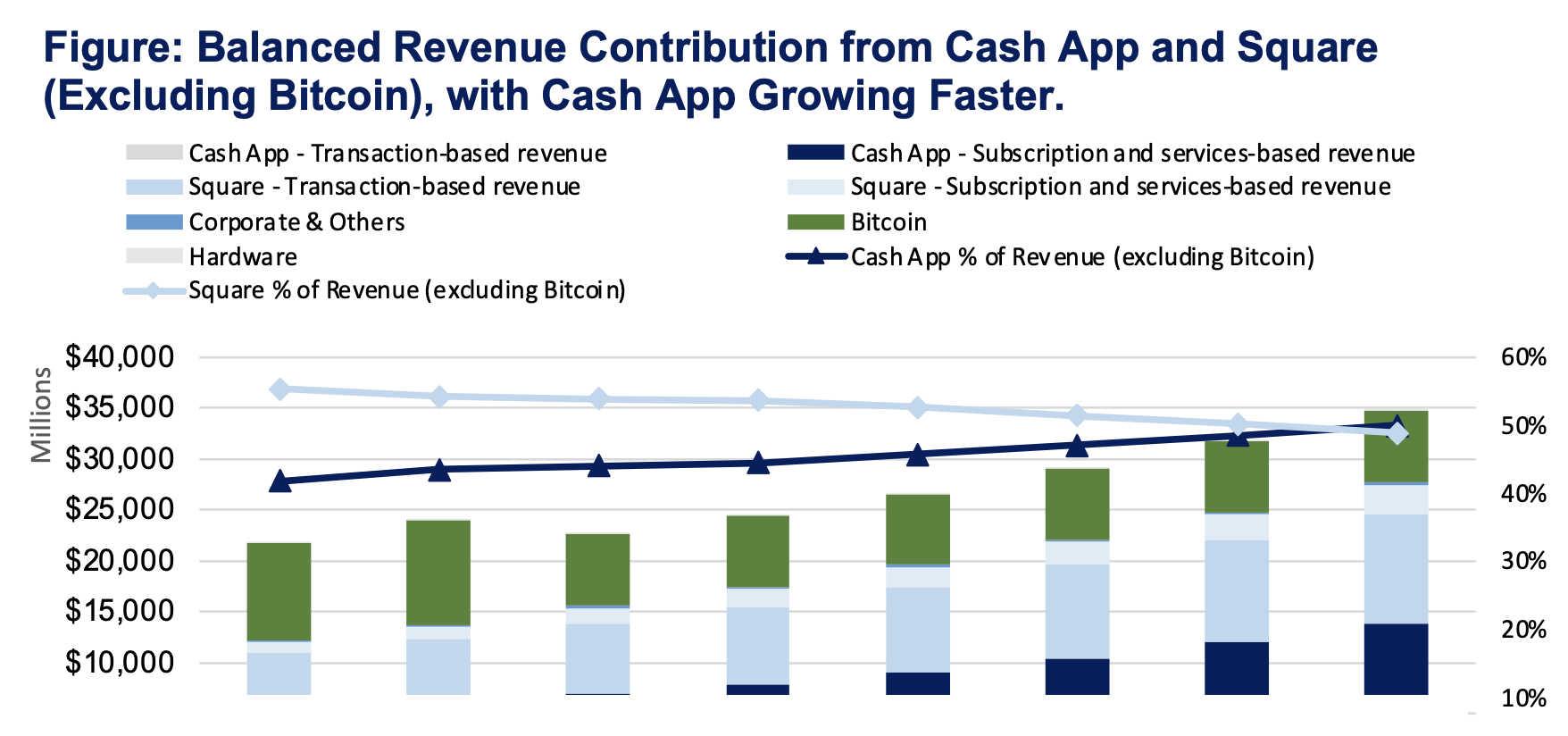

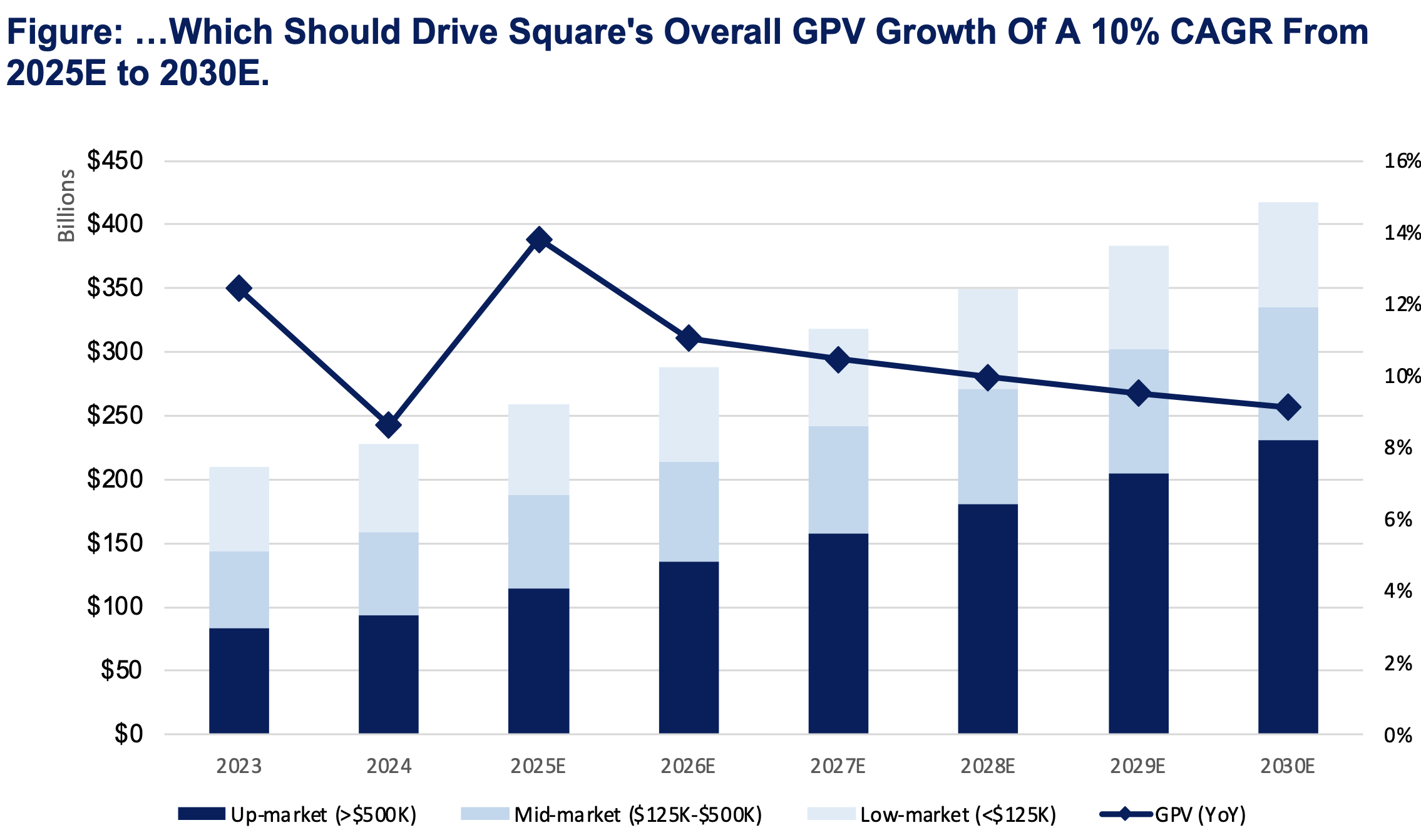

Square: Upmarket re-acceleration driven by GTM redesign and verticalization. Square is shifting from historically product-led self-onboarding to a sales-led, localized, vertical-specific GTM motion aimed at sellers >$500k GPV. This strategy is already reflected in mix-shift evidence: larger seller GPV share rose from 34% (1Q23) to 45% (3Q25).

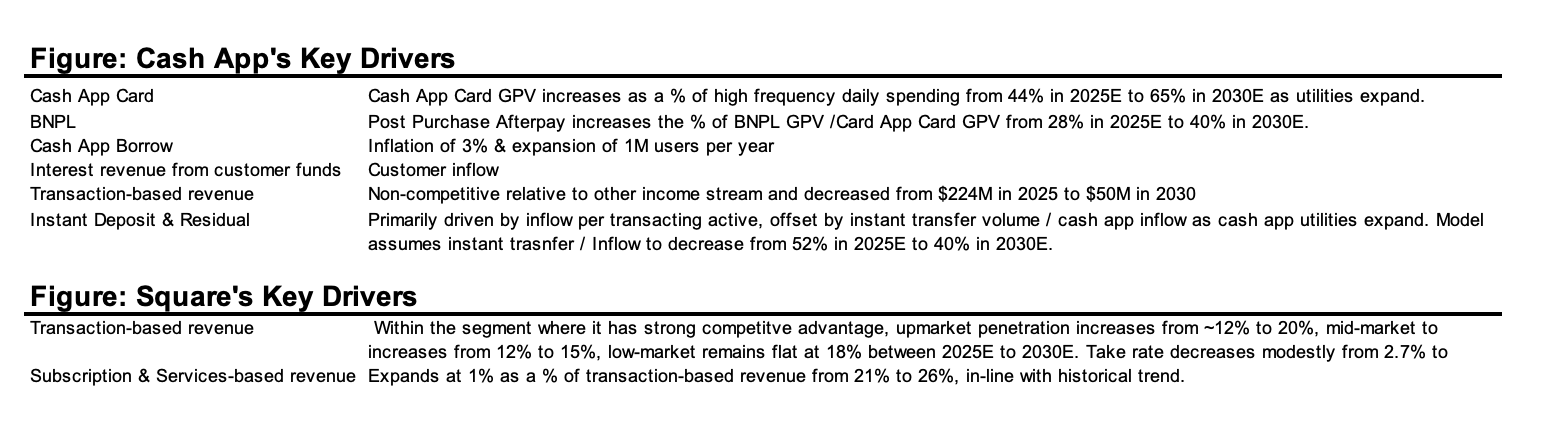

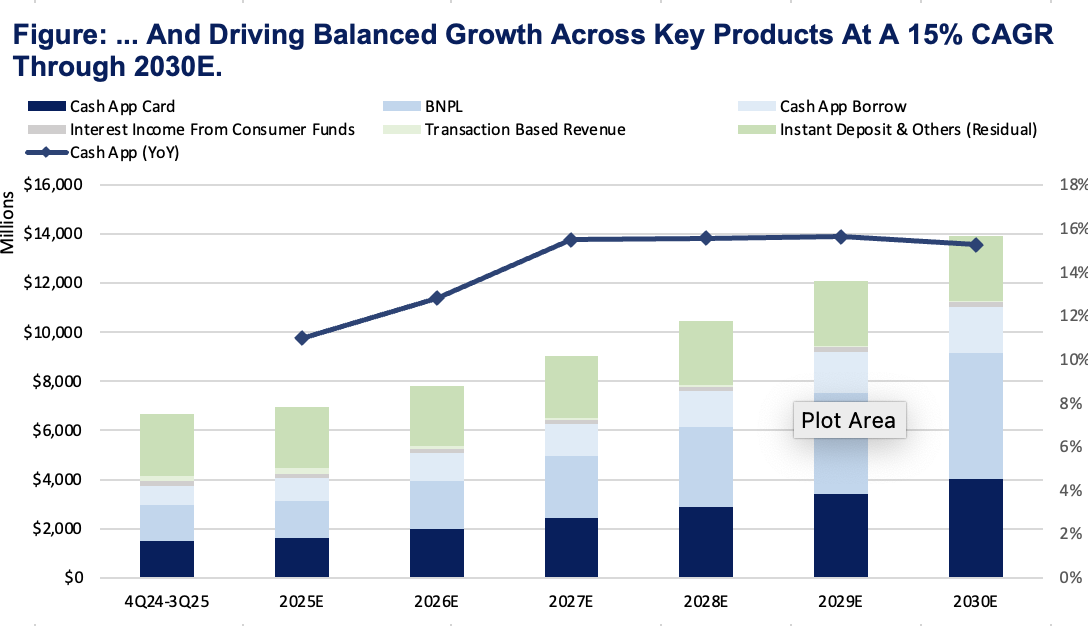

Cash App: P2P is the retention anchor; monetization is ARPU expansion via PFR capture. Cash App’s strategic objective is to migrate users from P2P utility to Principal Financial Relationship by winning inflows, increasing high-frequency spend utility (debit + BNPL), and expanding credit/lending usage where it solves liquidity timing mismatches. The “Gen Alpha” funnel (sponsored accounts) aims to lock in new cohorts at the point of financial habit formation, extending lifetime value and lowering blended acquisition costs.

Ecosystem synergy: Closed-loop is the margin unlock (but execution remains uncertain). Afterpay integration increases spend utility and keeps balances within Cash App, while Cash App Pay at Square merchants can internalize economics otherwise paid to networks/acquirers, converting a variable external toll into gross profit.

Section: Business Model

Block, Inc. is a fintech company that builds technology “to increase access to the global economy,” organized around two ecosystems: Square and Cash App.

Square

The Square segment has evolved from a niche card acceptance utility into a cohesive commerce operating system (OS). The value proposition has shifted from simple payment processing to a holistic suite enabling merchants to start, run, and scale operations across sales, personnel, and financial management.

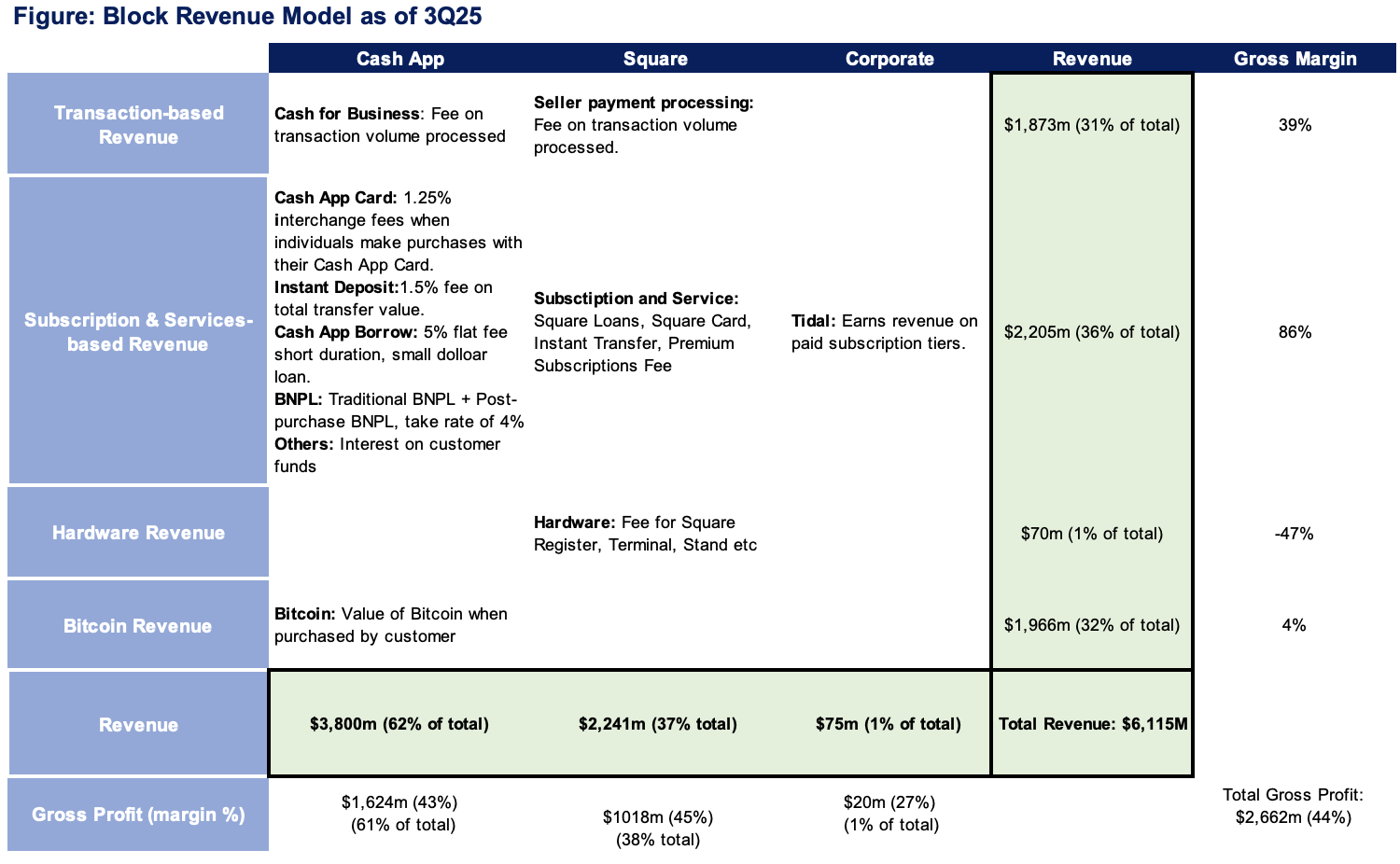

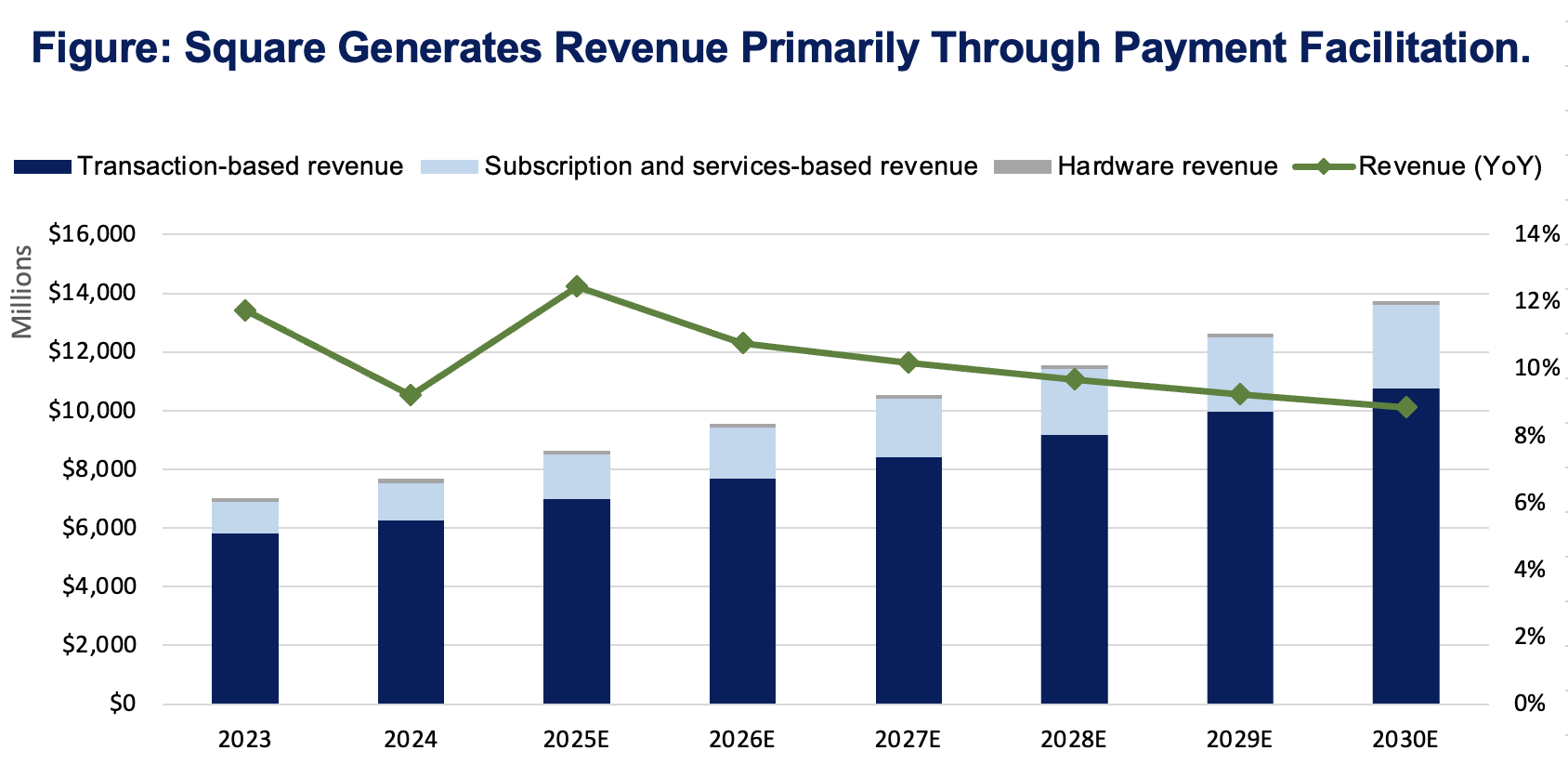

Revenue Mechanics. Square operates primarily as a Payment Service Provider utilizing a Payment Facilitator model. This allows Square to act as the merchant of record, effectively aggregating merchants under a master account to bypass the friction of traditional merchant account underwriting. Revenue is derived from three core streams:

Transaction-Based: Merchant processing fees (a percentage of Gross Payment Volume or GPV).

Subscription & Services: SaaS fees for vertical-specific software (Restaurants, Retail) and hardware.

Banking & Financial Services: Yield on Square Loans and instant transfer fees.

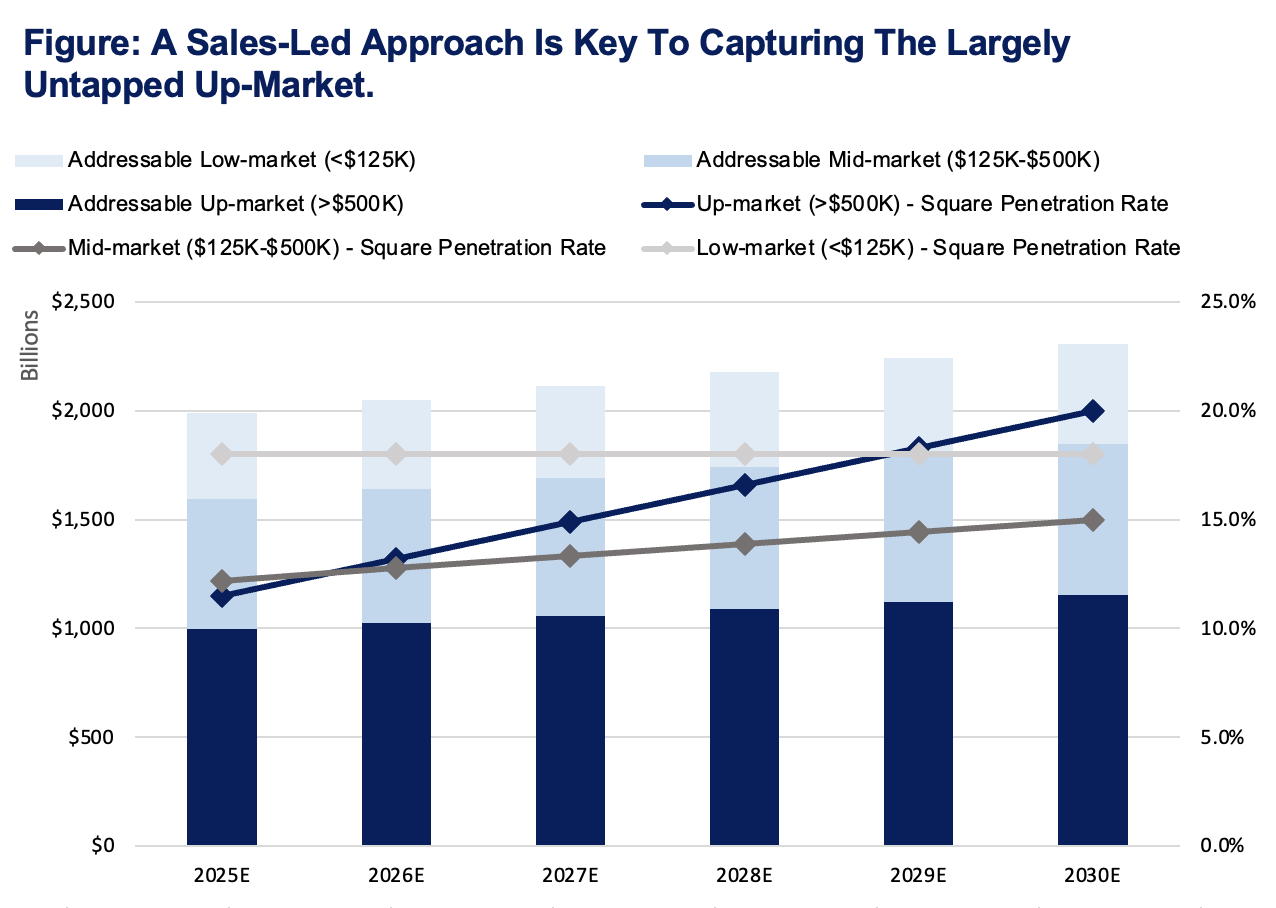

Strategic Pivot: Upmarket “Sales-Led” Evolution and Verticalization & The Banking OSHistorically reliant on product-led growth (self-onboarding). Square is aggressively reorganizing its Go-to-Market (GTM) motion to capture upmarket sellers (>$500k GPV). This is evidenced by the mix shift in GPV; mid-market sellers (>$500k annualized GPV) have grown significantly, contributing to the increase in larger seller GPV share from 34% in 1Q23 to 45% in 3Q25.

Localizing Sales: Mimicking the successful "territory model" of competitors like Toast, Square has shifted from generalist sales to localized, vertical-specific teams. This high-touch approach is critical for displacing legacy incumbents (Chase/Wells Fargo) in complex SMBs.

Incentive Alignment: Compensation structures have shifted to reward software attachment rates rather than just payment volume, driving deeper ecosystem lock-in.

Deep Vertical Stacks. The company creates stickiness through industry-specific ERP integrations (e.g., Square for Restaurants, Retail). This software layer acts as the "moat," while payments serve as the monetization engine.

Financial Services as Retention. By embedding banking products—Square Checking, Loans, and Payroll—Square creates a "high switching cost" environment. A merchant using Square for capital and payroll is statistically less likely to churn than one using it solely for payments.

Geographic Mix: US remains the core market (79% of Gross Profit in 3Q25, down from 85% in 3Q22).

Cash App

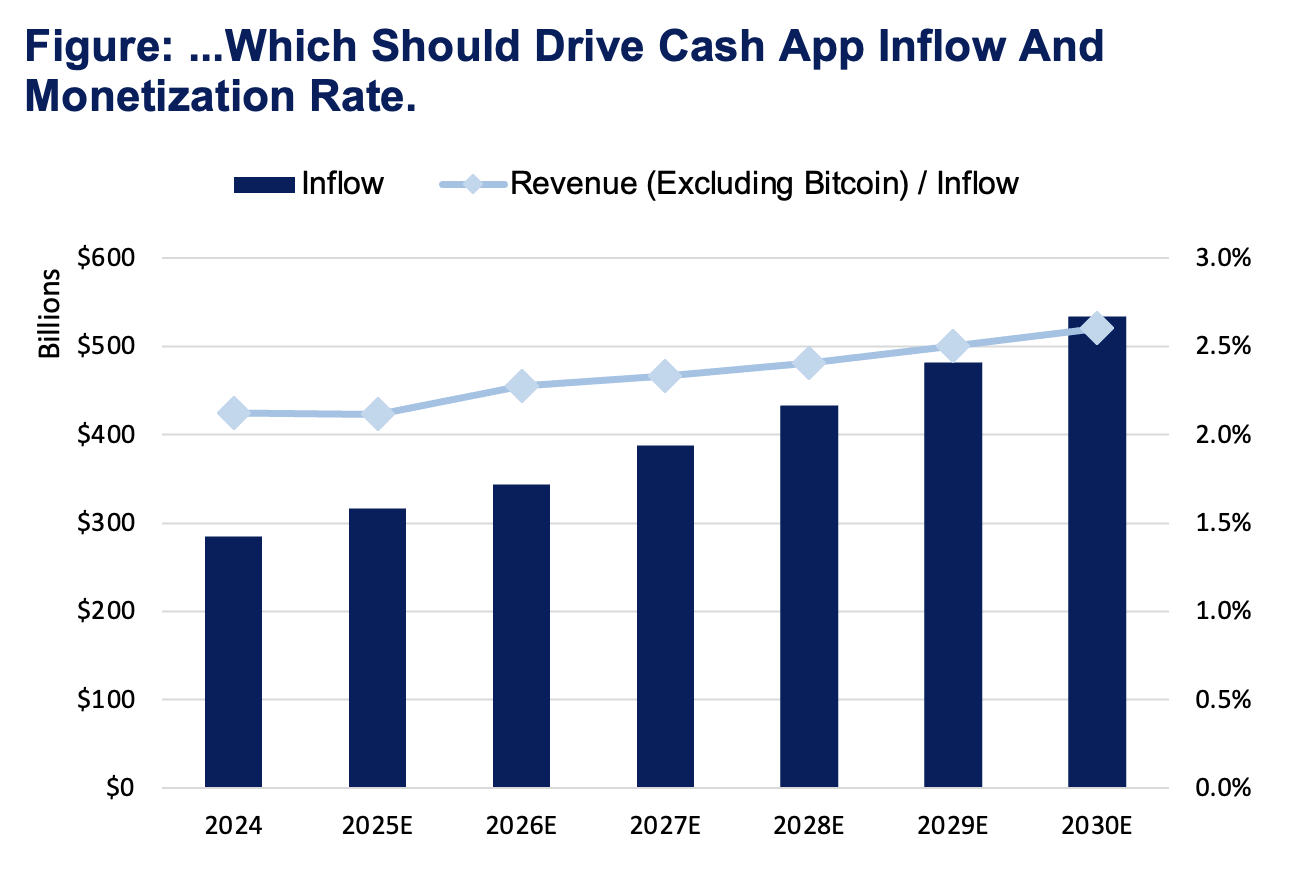

The core strategy is to transition users from P2P utility to Principal Financial Relationship. The unit economics are driven by the "usage velocity" flywheel: bridging a user from a peer-to-peer transfer to a banking product (e.g., Cash Card or Borrow) expands revenue per user by 2x–3x without incremental Customer Acquisition Cost (CAC).

Strategic Pillars for Inflow Growth

Direct Deposit Disruption: Cash App competes for the paycheck by offering 2-day early access, overdraft coverage, and high-yield savings. This effectively removes the need for a traditional DDA (Demand Deposit Account).

The "Gen Alpha" Funnel: The "Sponsored Account" strategy targets the pre-banked demographic (13–17-year-olds). With ~25M teens in the US and 1-in-5 already on the platform, Block is acquiring customers at near-zero CAC via their parents. As these users mature into financial independence (18+), they unlock full functionality with 5+ years of transaction history already established.

The integration of Afterpay serves as the bridge between "saving" and "spending." It solves the deposit side by increasing utility; users keep balances in Cash App to service BNPL installments. This creates a closed-loop ecosystem where Block captures value on both the funding (Cash App) and merchant settlement sides.

Cash App effectively monetizes the velocity of money within its walled garden. Key revenue drivers include:

Interchange: Earned on Cash App Card (debit card) transactions.

Services: Instant deposit fees (transferring to external banks) and interest income from Cash App Borrow.

Flywheel Dynamics: The debit card and BNPL (Afterpay) serve as high-frequency spending utilities; while investing and savings features act as retention mechanisms. This combination increases "inflows per active," transforming the app from a P2P tool to a primary banking substitute.

Cash App’s core demographic skews toward younger (Gen Z/Millennial) and lower-to-middle income consumers ($50k–$100k), often characterized by cash flow volatility.

The Credit Arbitrage: High adoption of Cash App Borrow (5.5x frequency) is not indicative of insolvency, but of liquidity timing mismatches. Users utilize the platform to bridge the gap between pay cycles. The seamless repayment mechanism (deduction from next inflow) lowers default risk relative to traditional unsecured lending.

Generational Wealth Transfer: While Gen Z comprises the largest user base (38% of actives) and exhibits high engagement, the "Power Users" are the 25–44 cohort, who drive 42% of inflows. The platform's inability to penetrate Gen X and Boomer cohorts remains (high income, low adoption) remains, who remain entrenched with legacy institutions.

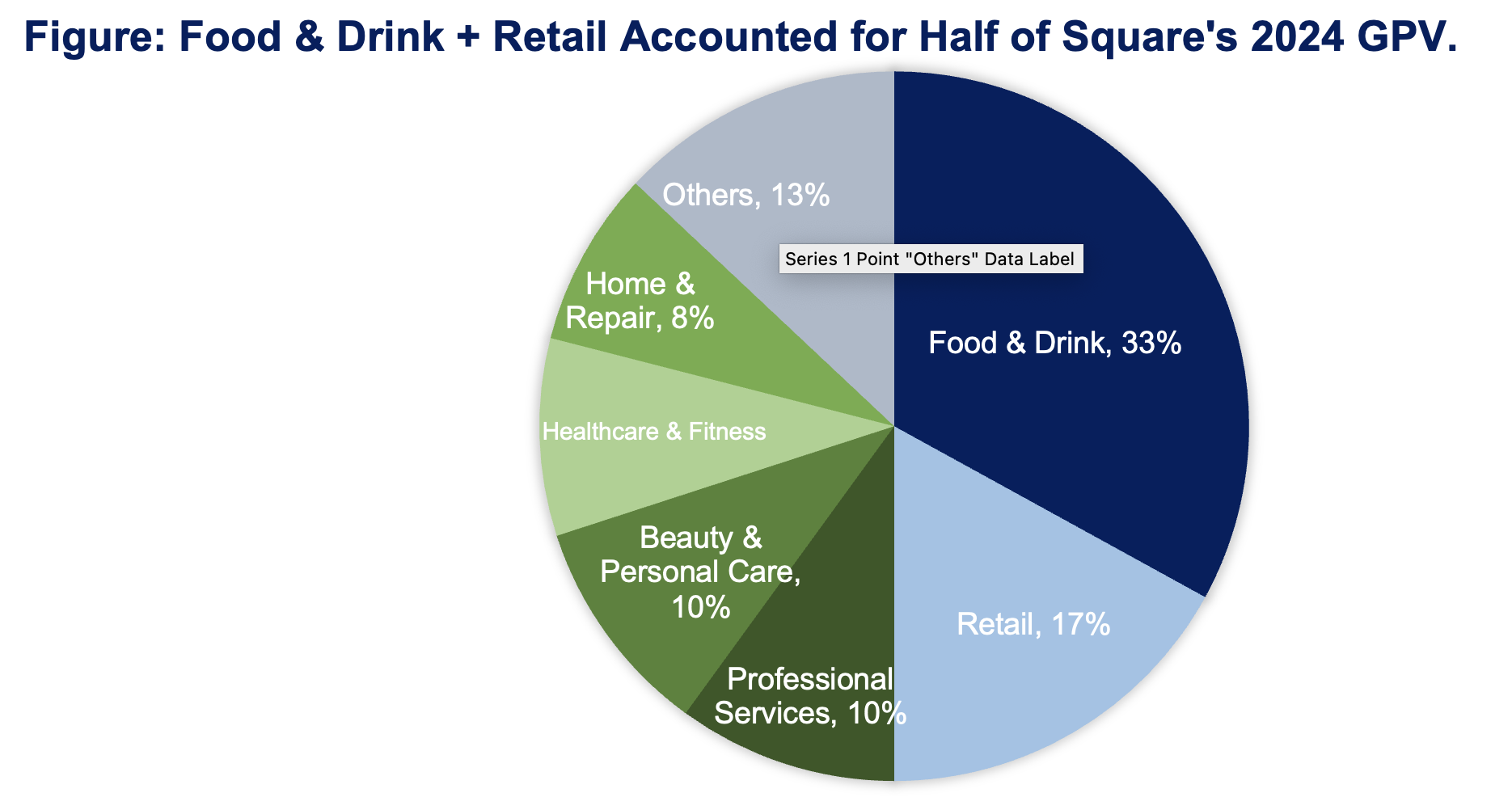

Spending Behavior. Cash App Card usage reflects "essential" spend rather than discretionary luxury. 2023 data indicates a concentration in big-box retail (22%) and dining (19%). With average annual spend around $5,700, Cash App currently serves as a secondary, discretionary wallet rather than the primary demand deposit account (DDA) for the majority of users.

Other Segment

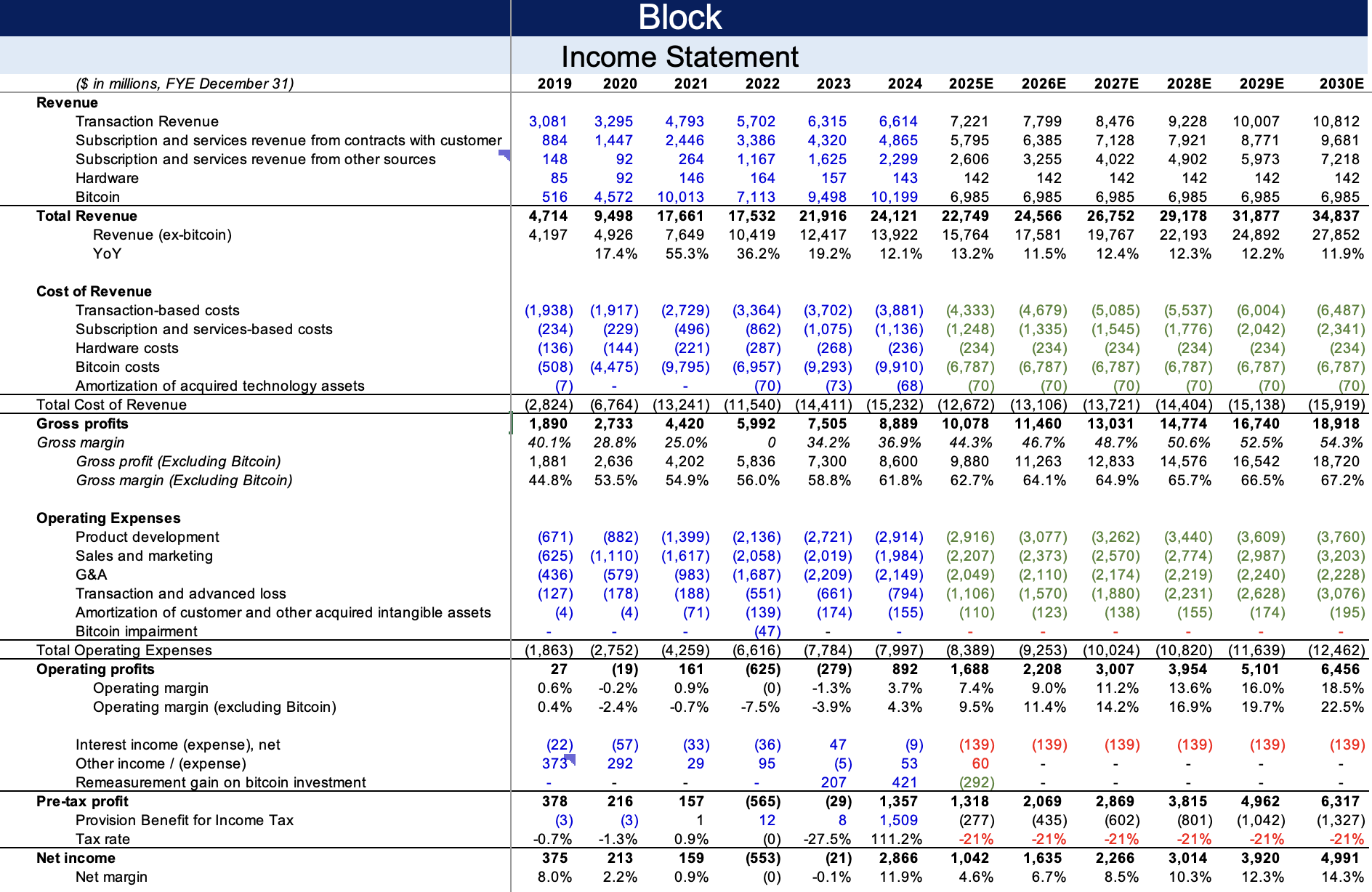

Bitcoin. Bitcoin revenue serves as a low-margin customer acquisition tool (CAC efficiency) rather than a profit driver. Revenue acts as a pass-through (recognizing the gross value of Bitcoin sold), while Gross Profit reflects the small spread (usually <2%) charged on trades. This segment introduces volatility correlated with crypto cycles but enhances ecosystem engagement.

Others (Primarily TIDAL). Tidal operates as a vertically integrated artist-services platform. While currently a minor contributor to the bottom line, it provides potential synergies for creator-economy financial tools within the broader Block ecosystem.

Ecosystem Synergy

Block’s end game rests on connecting its two distinct ecosystems to create a closed-loop economy, which could boost significant margin expansion by cutting out interchange fee pays to network or acquirer / processor fees. Block has taken initiatives below but result remains highly uncertain.

Local Discovery Engine: Utilizing Cash App’s interface to surface Square merchants creates a lead-generation engine for sellers.

Cash App Pay: By incentivizing Cash App users to pay at Square merchants (via Boosts or discounts), Block eliminates card network fees (Visa/Mastercard), effectively internalizing the transaction margin and improving gross profit profiles for the consolidated entity.

Section: Industry Analysis

Square App

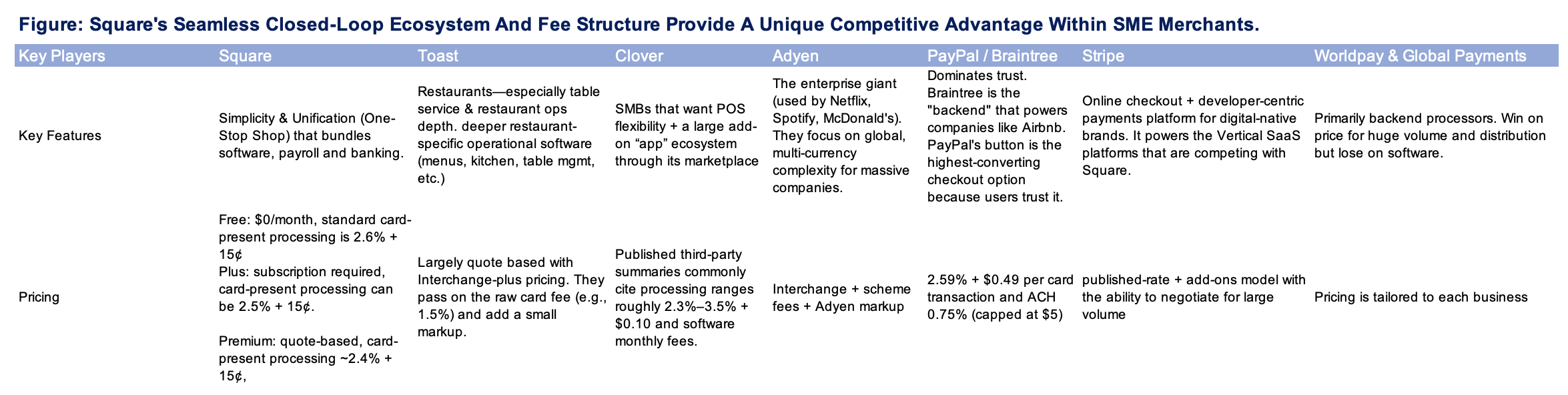

The payment processing market has bifurcated into distinct lanes based on merchant size and origin (online vs. offline). Generally speaking, players within Enterprise Segment are commoditized business that competes primarily on pricing.

Enterprise (>$20M GPV): Square faces structural headwinds here. Large merchants typically demand "Interchange Plus" pricing (cost + ~0.05%) and bespoke API integrations. Square’s flat-rate model and closed ecosystem are often deal-breakers for global enterprises, who favor Adyen (unified commerce) or Stripe (developer-first customization).

SMB & Mid-Market (<$20M GPV): This remains Square’s battlefield. The competitive advantage lies in the "One-Stop Shop" value proposition—bundling payments, payroll, banking, and software into a single dashboard. This integration lowers total cost of ownership (TCO) for merchants compared to stitching together 3–4 separate SaaS providers.

Vertical-Specific Competition

A. Restaurants (<$5M sales, 75% of the overall market):

Toast (17% market share): Holds the advantage in "depth" (specialized Kitchen Display Systems, deep inventory management).

Clover (20% market share): Glover adopts a large add-on “app” ecosystem through its marketplace.

Square (13% market share): Wins on "breadth" (ecosystem banking, loans, payroll). Square is effectively defending the Quick Service Restaurant (QSR) and cafe segment, while Toast dominates full-service dining.

B. Retail:

Shopify: The default for "Digitally Native" brands moving offline.

Square: The default for "Physical Native" retailers moving online.

C. Services & General SMB:

Clover (Fiserv): Relies on a legacy Distribution Moat. Fiserv leverages thousands of bank partnerships (e.g., Bank of America, Wells Fargo) to push Clover hardware as the default option for business banking clients.

Square: Relies on a Product Moat. Square wins when merchants actively seek a better software interface, whereas Clover wins when merchants passively accept what their bank offers.

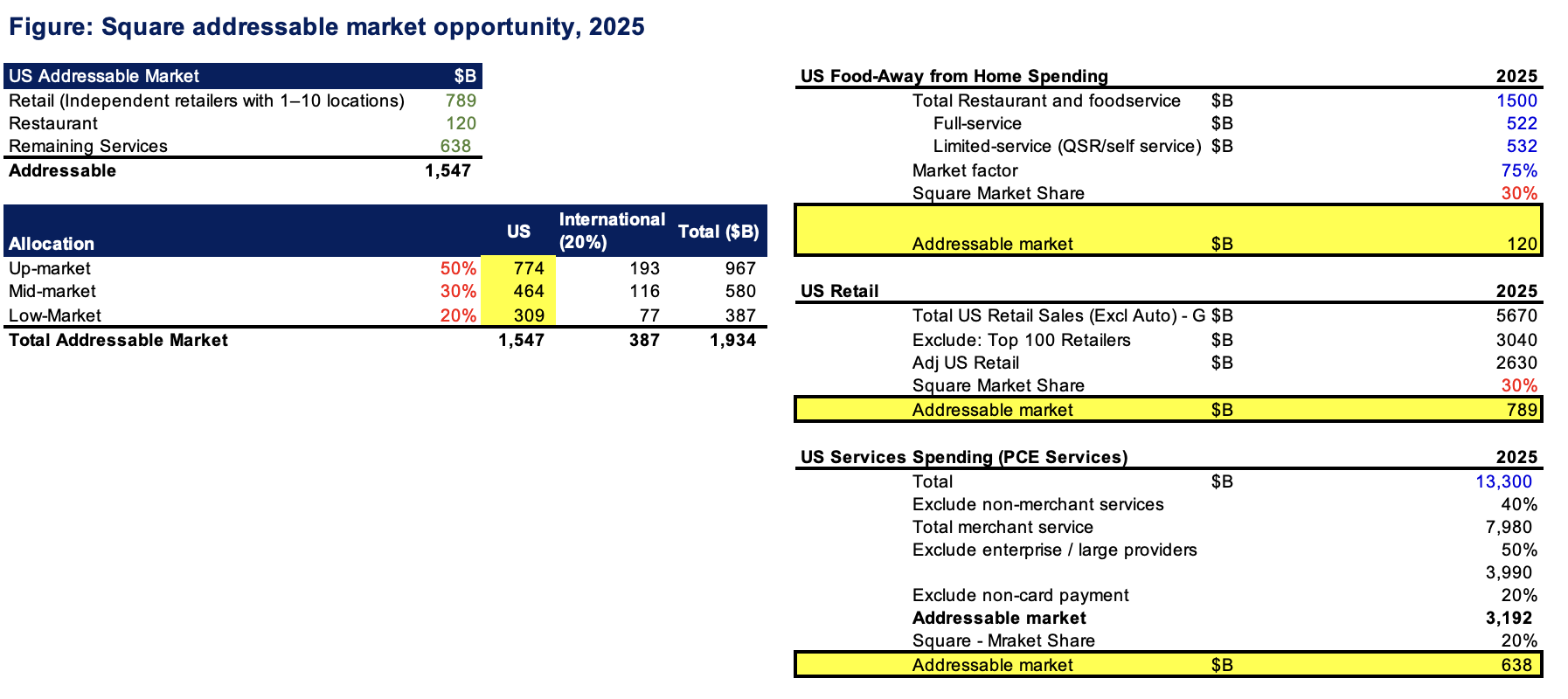

Total addressable market of $1.9T for Square App across US and International footprints. With current penetration at roughly ~13%, growth will no longer come from passive adoption but from the new "outbound sales" motion targeting the "sweet spot" of merchants with >$500k in GPV who are underserved by legacy acquirers but too small for Adyen.

Cash App

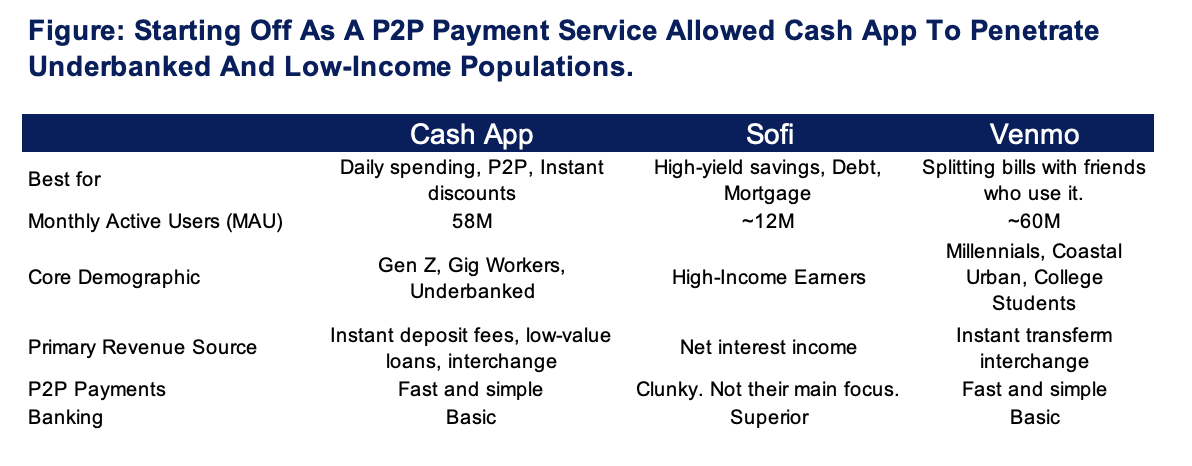

Cash App competes for the high-frequency transactional wallet of the younger and underbanked demographic. Increase in high-frequency transactions could improve inflows and ultimately other banking products.

The Rewards Gap: Cash App cannot compete on rewards v.s. credit cards. An affluent user spending $3k/month earns ~$720/year on a 2% cashback credit card. Cash App Boosts (merchant-funded, sporadic) yield significantly less (~$90/year).

The Liquidity Advantage: Cash App wins on liquidity velocity. For a Gig Economy worker or Gen Z consumer living with cash flow volatility, "rewards" are secondary to "access." Features like 2-day early pay and Cash App Borrow provide immediate utility that traditional credit cards (which require prime credit scores) do not offer.

Gen Z is structurally unbundling their financial lives. They utilize legacy banks as a "Storage Vault" for bulk savings but utilize fintechs (Cash App/Venmo) as the "Daily Wallet."

The Gig Economy Tailwind: The US Gig Economy ($1.3T Gross Volume) is dominated by Gen Z/Millennials (62%). These workers have a mismatch between income frequency (often bi-weekly) and expense frequency (daily). Cash App bridges this gap.

Demographic Saturation: With ~58M Monthly Active Users (MAUs) against a core demographic of ~140M US Gen Z/Millennials, broad user acquisition is likely slowing. The growth narrative has shifted from "User Growth" to "ARPU Expansion."

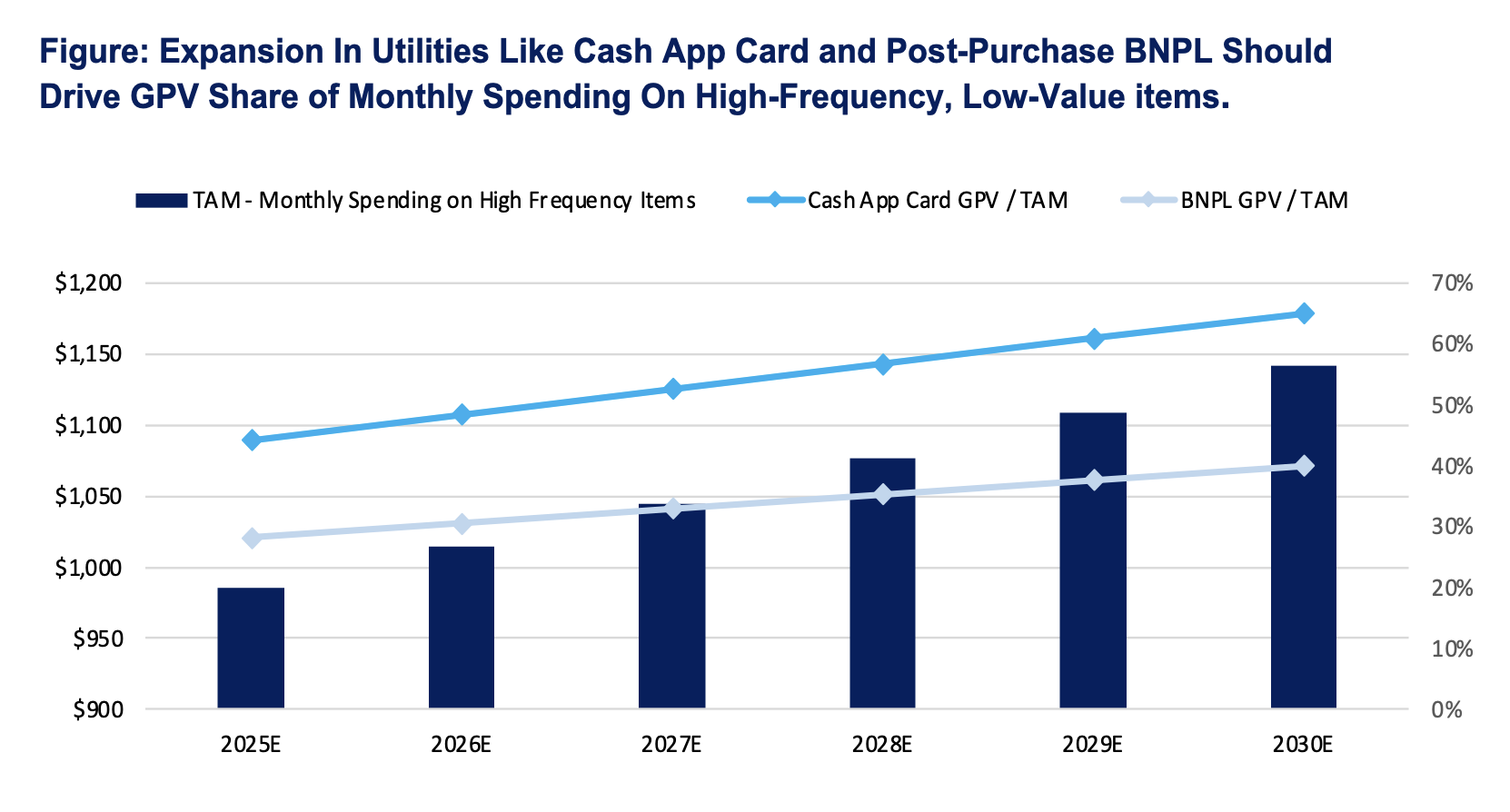

Current Capture: Young consumers spend ~$985/month on high-frequency essentials. Cash App Card currently captures ~$436/month (44% share of wallet) for active users.

The BNPL Unlock: The Afterpay integration is the primary vehicle to capture the remaining 56% (discretionary spend). By extending credit at the point of sale, Block moves up the spending funnel, capturing volume that would otherwise go to credit cards.

Section: Value Proposition

Square creates value by (a) unifying the Payment Utility with the Banking Layer, (b) decreasing total cost of ownership & accessibility and (c) utilizing its network advantage from Cash App.

Instant Access. A merchant utilizing Square Checking receives sales proceeds instantly (including weekends), effectively zeroing out the "float" time, while competitors typically charge a 1.5%–1.75% fee for "Instant Payouts." For a merchant with $50k in urgent working capital needs annually, Square’s native integration saves ~$750–$900 in fees—a material margin improvement for low-margin businesses.

The "Unbundled" Arbitrage: Traditional merchant acquiring requires stitching together a patchwork of vendors (Gateway + POS + Payroll + Banking), often with opaque contract terms and monthly SaaS fees ($69+). Square’s "Freemium" software model with transparent flat-rate processing lowers the barrier to entry, capturing the "Long Tail" of merchants that legacy acquirers ignore.

Revenue Synergies: The integrated ecosystem drives topline growth. Internal data suggests seller cohorts adopting the broader software suite (e.g., Marketing, Loyalty) generate ~9% higher sales than standalone peers, validating the "ecosystem uplift" thesis.

The Network Advantage. Square leverages its consumer arm (Cash App) to lower Customer Acquisition Cost (CAC) for merchants. By surfacing local Square merchants within the Cash App interface, Square provides a "free" marketing channel that competitors like Clover or Toast cannot replicate without a consumer-facing platform.

Cash App creates value by solving the timing mismatch between Income (Bi-weekly) and Consumption (Daily), accessibility to banking, aligned incentives for gig workers and young cohort.

Gig Economy Integration: For the independent workforce (Uber, DoorDash), Cash App integrates directly with "Instant Pay" platforms. This demographic values immediate liquidity over interest rates.

The "Bridge" Product: Cash App Borrow functions as a short-term liquidity bridge rather than a long-term debt instrument. It allows solvent but illiquid users to smooth consumption volatility without resorting to predatory payday loans or overdraft fees.

Low floor banking. Traditional banks impose minimum balance requirements and maintenance fees that penalize low-balance accounts. Cash App’s fee-free structure (monetized via interchange and instant transfers) effectively subsidizes the banking cost for the underbanked.

Credit building. The ecosystem offers a "Credit Ladder" for thin-file consumers. By utilizing Cash App Pay (BNPL) and Borrow, users access credit utility without the risk of revolving debt traps associated with traditional credit cards.

Aligned incentives differs from tradition Ing banking. Unlike legacy credit issuers that profit from consumer error (late fees, compounding interest), Cash App’s credit products (Borrow/Afterpay) are structured around flat transaction fees and capped exposures. This "Fee Transparency" resonates with a Gen Z demographic that is structurally averse to revolving credit debt.

The Unified Financial Interface: Cash App differentiates through extreme reduction of friction. By consolidating disparate financial verticals—P2P payments, equity/Bitcoin investing, direct deposits, and tax filing—into a single, mobile-first interface, Block removes the "cognitive load" associated with traditional banking silos.

The P2P Anchor: Peer-to-Peer transfer functionality serves as the high-frequency "social hook" that keeps the app top-of-mind. This social utility creates a daily engagement habit, which Block then leverages to cross-sell lower-frequency, higher-margin banking products (e.g., the Cash Card) within the same "low-friction" ecosystem.

Section: Business Moats & Risks

Evidence of Moats

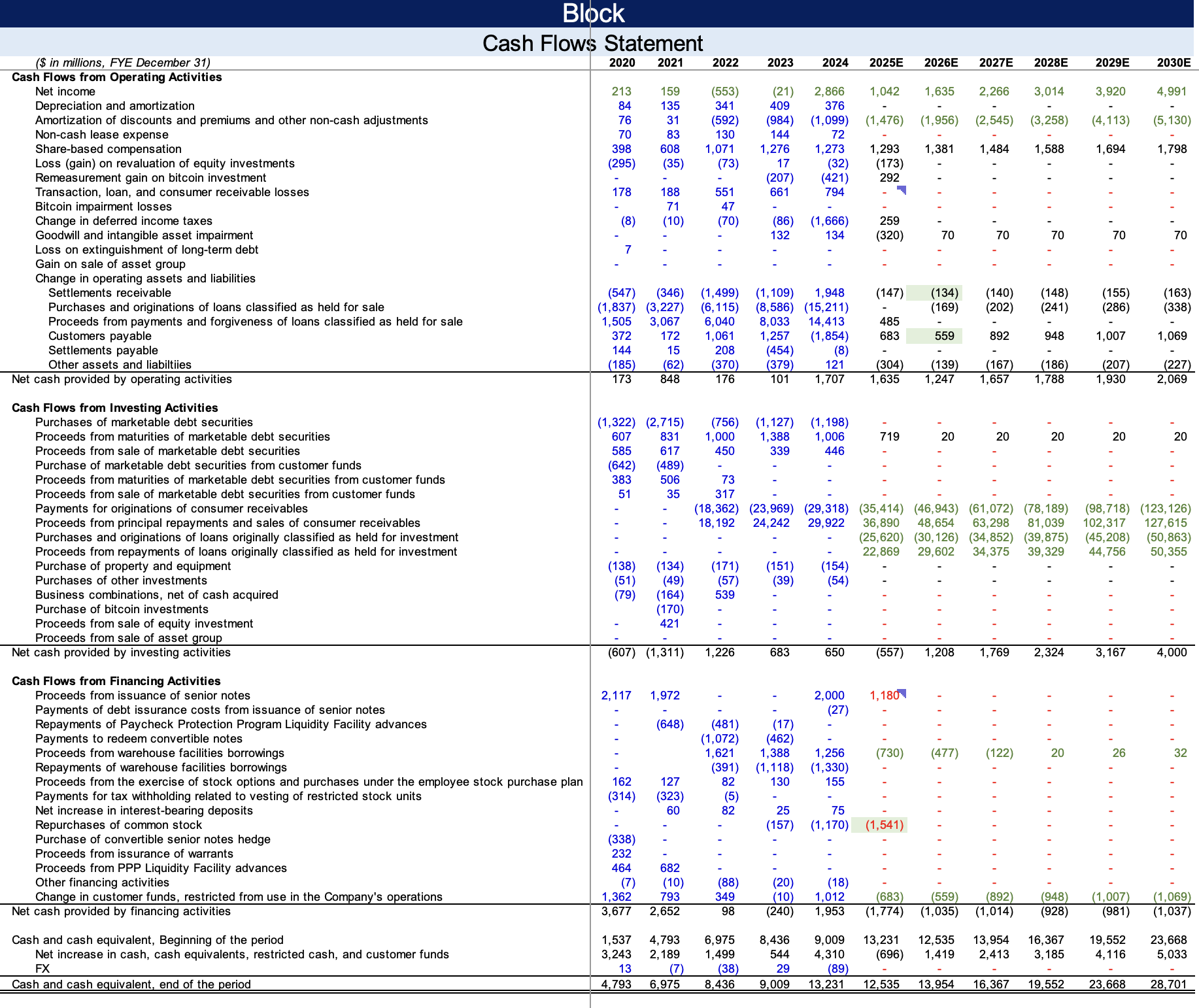

Expanding ROIC from -6% in 2022 to 10% 3Q25 (annualized).

Strong adaptation in recently launched Cash App products (Cash App Borrow and Cash App post-purchase Afterpay.

Consistent market share gain for Square.

Improving operating margin (excluding Bitcoin) from -8% in 2022 to 8% in 3Q25.