LendingClub (NYSE: LC)

Executive Summary

LendingClub is a manufacturer of commoditized unsecured consumer loans permanently squeezed between aggregators who own the borrower relationship and institutional buyers who set the clearing yield. Because all lenders compete on the same comparison screens simultaneously, any underwriting or funding advantage is immediately weaponized to win volume rather than retained as excess profit, leaving the originator with structurally limited pricing power.

Boxed into the middle-prime Niche. The company is strategically trapped: it lacks the free depositor data and zero-fee model required to compete against traditional banks and SoFi at the super-prime level, and it is not data-nimble enough to out-underwrite AI-driven competitors like Upstart at the bottom of the credit spectrum. LendingClub's only viable hunting ground is the narrow band of over-leveraged, middle-prime debt consolidators that larger institutions deem slightly too risky.

Minimal market share gain over the long-term. Despite holding a bank charter and maintaining superior loss rates, LendingClub's share of total US unsecured personal loan originations—including within its own target prime, prime-plus, and near-prime segments—has remained static and range-bound for years. If a genuine structural cost advantage existed, basic economics dictates the company would be eating the market. It has not.

The company's volatile financial performance reflects a fundamentally constrained business with no protective moat. Return on Equity fluctuated between -23% and 9.5% from 2019 to 2025, and their 40% origination growth in late 2025 represented merely a cyclical recovery from a depressed base.

Valuation: A Graham-Style Cigar Butt at Reproduction Value of $12.4. Because the company operates a commodity business generating returns that merely hover near its cost of equity over a full cycle, the only intellectually honest valuation framework is a discount to reproduction value. I value the business at $12.4 per share, representing net assets adjusted for goodwill, the cost to obtain the banking charter, and outstanding options and RSUs. A high margin of safety is non-negotiable given the combination of cyclical earnings volatility, and severe downside tail risk.

Business Model

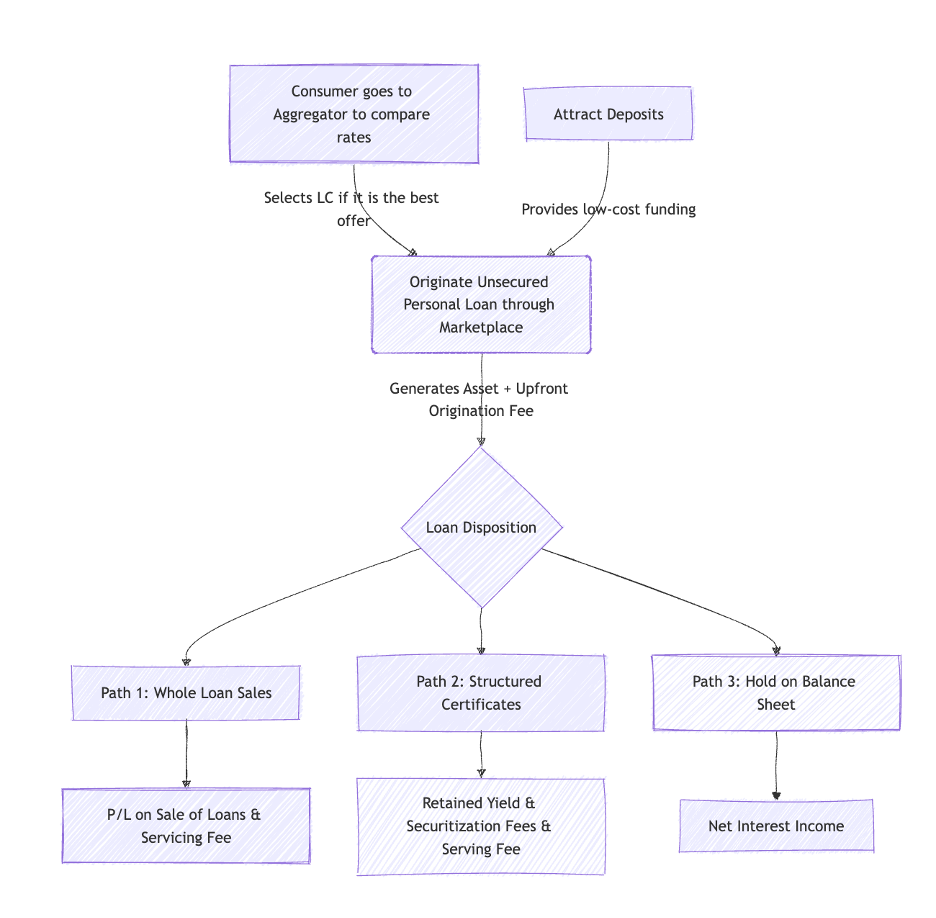

Commoditized Loan Manufacturing. LendingClub operates as a manufacturer of highly commoditized unsecured consumer loans. The company relies on third-party aggregators for loan distribution and depends on institutional buyers or depositors to supply its funding.

Middle-Prime Underwriting. The company intentionally targets safe, "middle-prime" borrower segments that traditional FICO scores often overlook. By maintaining strong credit performance, LendingClub can charge lower interest rates while preserving high origination fees. This underwriting capability serves as a baseline survival requirement for its origination fee business model.

Bank Charter Advantages. Holding a national bank charter provides LendingClub with access to cheap, sticky deposit funding and balance-sheet flexibility that pure marketplace peers lack. However, this structural cost advantage does not guarantee outsized returns, especially if asset yields decline or credit losses spike during an economic downturn.

Structured Certificates Vulnerability. The company launched structured certificate programe on top of whole loan sale program in order to expand its funding sources.The company retains the senior notes of its loans while selling the levered, residual pieces to asset managers. This financial engineering carries immense tail risk because a severe credit cycle could easily wipe out these levered buyers. If these asset managers are wiped out, it would instantly destroy LendingClub's funding pipeline and broader reputation.

Overcapitalization Dilemma. LendingClub ended 2025 heavily overcapitalized with a 17.4% Common Equity Tier 1 ratio, far above the typical 9% to 11% held by traditional banks. Lower interest rates temporarily boost the fair value of existing loans, but they simultaneously trigger prepayments that cannibalize future net interest income. This dynamic limit sustainable origination growth and forces management to rely heavily on stock buybacks to deploy their excess capital. In November 2025, they authorized a $100 million stock repurchase program specifically to chip away at this excess capital.

Fundamental Contraints to Scale.

The Deposit Constraint: To retain more loans, LendingClub must raise matching deposits. Aggressively chasing loan growth simply to deploy trapped equity would force them to offer higher interest rates to attract hot money.

The Credit Quality Constraint: If the company forces loan growth beyond what its strict credit box naturally produces, it must lower underwriting standards. Doing so would destroy the "better credit performance" advantage it uses to lowers gross interest rate, inviting disastrous tail risk.

The Regulatory Reality: While traditional banks safely operate at 9% to 11% CET1 ratios because their balance sheets hold diversified, low-risk assets like government bonds (0% RWA), LendingClub is essentially a monoline lender concentrated in volatile unsecured debt (100% RWA). Standard risk weightings arguably underestimate the true tail risk of a portfolio with zero collateral, forcing management to artificially maintain a massive 17% CET1 buffer to prevent regulatory intervention.

Industry Dynamics

The Shrinking Cost Advantage. As lenders move down the credit spectrum, the primary driver of profitability shifts rapidly from the cost of capital to the cost of defaults. At the super-prime level, defaults approach zero, meaning cheap bank deposits are the only competitive differentiator—an arena where traditional banks hold a permanent advantage. Further down the spectrum into near-prime and sub-prime segments, defaults become the dominant expense.

The Middle-Prime Squeeze. This dynamic completely boxes LendingClub into the "middle-prime" debt consolidator niche. They lack the free data, zero acquisition costs, and rock-bottom deposit pricing required to beat traditional banks or SoFi for super-prime borrowers. LendingClub and other fintechs are essentially fighting over the "leftovers"—borrowers who were rejected by their primary banks or those demanding a frictionless digital experience. Meanwhile, it is unlikely that Fintech can move upmarket due to their higher cost of funding.

Credit Segmentation. The industry has clearly stratified based on algorithmic risk tolerance and cost of capital.

Traditional Banks & SoFi: Dominate the super-prime segment using zero-fee models funded entirely by cheap deposits.

LendingClub: Captures the over-leveraged "middle-prime" debt consolidators by accepting slightly higher debt-to-income ratios while leveraging its bank charter for cheaper capital compared to pure-play fintechs.

Upstart: Operates in the near-prime and sub-prime space, utilizing AI models to find hidden approvals while charging significantly higher rates to offset the elevated default risk.

Value Proposition

Institutional Buyers (Whole-loan and structured buyers)

Loan Sourcing. LendingClub operates as an outsourced loan origination platform for whole-loan and structured certificate buyers. It handles underwriting and marketing at scale, delivering consistent prime consumer credit in exchange for a 1% servicing fee on payments received. Because it is costly for asset managers to originate large volumes of loans internally, they sign "Forward Flow" agreements with LendingClub to secure a massive, predictable firehose for capital deployment.

Solving Institutional Trust. The platform solves a fundamental trust issue inherent in secondary loan purchasing. Traditional banks typically hold their best prime paper to collect safe interest, offloading only their lower-tier originations to the open market. LendingClub retains roughly 15% to 25% of the exact same prime loans on its own balance sheet. This alignment ensures management is eating their own cooking, giving buyers confidence that the company is not merely selling its lowest-quality assets..

Bespoke Credit Filtering. Institutional buyers on the platform are not forced to purchase a blind pool of loans. The system allows institutions to programmatically define their exact risk appetite.

Borrowers

Borrower Convenience. For consumers, the primary value is convenience and approval-fit for a specific "crossover" prime cohort. LendingClub targets high-income, high-credit-usage individuals seeking debt consolidation, offering average APRs of 16% compared to the 23% typically charged by credit cards. The company successfully captures prime borrowers who are deemed slightly too indebted by zero-fee traditional banks, providing an essential lifeline when cheaper lenders reject them.

Depositors

Depositor Yields. Through its bank charter, LendingClub offers a digital banking relationship that rewards depositors with market-competitive yields. In return, this supplies the company with a stable base of low-cost deposit funding that many pure-play fintech competitors fundamentally lack.

Business Moats

LendingClub operates in a commoditized market where borrower acquisition is completely transparent and comparison-driven. The company is perfectly squeezed between consumers demanding the lowest possible APR and institutional buyers requiring high risk-adjusted yields. Ultimately, it is extremely difficult to generate excess return in the long term.

The Plumbing Over the Product. Customer loyalty in unsecured lending resides entirely with the aggregators. The winner is simply the cheapest acceptable offer, not the best brand. Therefore, LendingClub lacks a moat in the actual product (the loan). If they possess any moat at all, it exists merely in their two-sided marketplace plumbing, which efficiently manufactures $10 billion worth of loans annually. Because excess benefits all go to the customers, LendingClub return on equity struggles to consistently exceed their cost of capital in the long term.

Empirical Evidence of Constraint. The company's volatile financial performance reflects a fundamentally constrained business with no protective moat. Return on Equity fluctuated between -23% and 9.5% from 2019 to 2025, and their 40% origination growth in late 2025 represented merely a cyclical recovery from a depressed base. More importantly, LendingClub's unsecured personal loan originations as a percentage of the total US market have remained static and cyclical, effectively trapped in a box.

Even when isolating for their specific target demographics—prime plus, prime, and near-prime borrowers—their market share exhibits the exact same stagnant fluctuation. If LendingClub genuinely possessed a structural cost advantage through its bank charter or underwriting, basic economic theory dictates they would systematically capture market share and eventually dominate the space. The reality that they have failed to eat the market—instead remaining bounded within a narrow historical range—serves as definitive empirical proof that no durable competitive advantage exists.

Debate: Whether LendingClub could meaningfully generate excess returns if it simply lowered their heavily overcapitalized 17% CET1 ratio?

View: This overcapitalization is an inherent constraint of unsecured lending. Unsecured consumer credit is one of the most volatile asset classes in banking, and a severe recession could spike loss rates dramatically. In addition, traditional banks can safely operate at a 9% to 11% CET1 ratio because their balance sheets are highly diversified. By contrast, LendingClub is essentially a monoline lender entirely concentrated in unsecured consumer debt. Because a standard 100% risk weight arguably underestimates the true tail risk of a portfolio with zero collateral to recover in a recession, management must artificially maintain a massive 17% CET1 buffer.

Valuation Methodology

LendingClub is fundamentally trapped in a static box where dropping fees destroys its Return on Equity (ROE), and lowering credit standards terrifies its institutional loan buyers. Because the company operates a commodity business devoid of a durable competitive advantage and generates returns that merely hover near its cost of equity, the only correct valuation framework must be strictly based on its tangible reproduction value.

Intrinsic value of $12.4. Represents Net Assets – Goodwill + Cost to Obtain Banking Charter ($50M) – Options & Restricted Stock Units Value ($83M)

The stock must be treated as a Benjamin Graham-style "cigar butt" that warrants a particularly high margin of safety as the reproduction value is highly sensitive to credit cycle.

Key Risks

The Cyclical Engine Stall. If the credit cycle turns and asset managers stop buying residual loans, LendingClub's origination fee engine will stall entirely. The company would be forced to hold loans more than intended on its balance sheet (exposed to high credit risks than intended) or drastically shrink its origination volume. This represents the primary cyclical risk to the business model.

Historical Precedent of Credit Shocks. During the 2008-2010 Great Financial Crisis, the Federal Reserve reported that average consumer loan charge-offs peaked at 7%. However, unsecured personal loans inherently carry more risk than average consumer debt. Charge-off rates for this specific asset class routinely exceeded 10% to 12% during the crisis peak.

LendingClub ended 2025 with $11.6 billion in total assets, backed by $1.5 billion in total equity and an overcapitalized 17.4% CET1 ratio. If a similar credit shock occurred today, the business would suffer a simultaneous two-front attack:

Balance Sheet Contagion: LendingClub retains a portion of its originations on its own balance sheet. If charge-offs on a hypothetical $3 billion retained portfolio spiked by 600 basis points—jumping from a normalized 6% to 12%—it would generate $180 million in unexpected annual credit losses. Because the company currently generates roughly $166 million in annualized net income, this excess loss alone would completely wipe out earnings and push the bank into a net loss:

Marketplace Liquidity Collapse: An even more severe risk lies in the loans LendingClub does not retain. During a financial panic, institutional buyers and asset managers flee risky unsecured consumer debt. If these buyers disappear, LendingClub's origination volume and fee revenue would instantly collapse, leaving the company with an oversized cost structure and evaporating cash flow.